Salary Sacrifice Explained

Last reviewed: April 2026

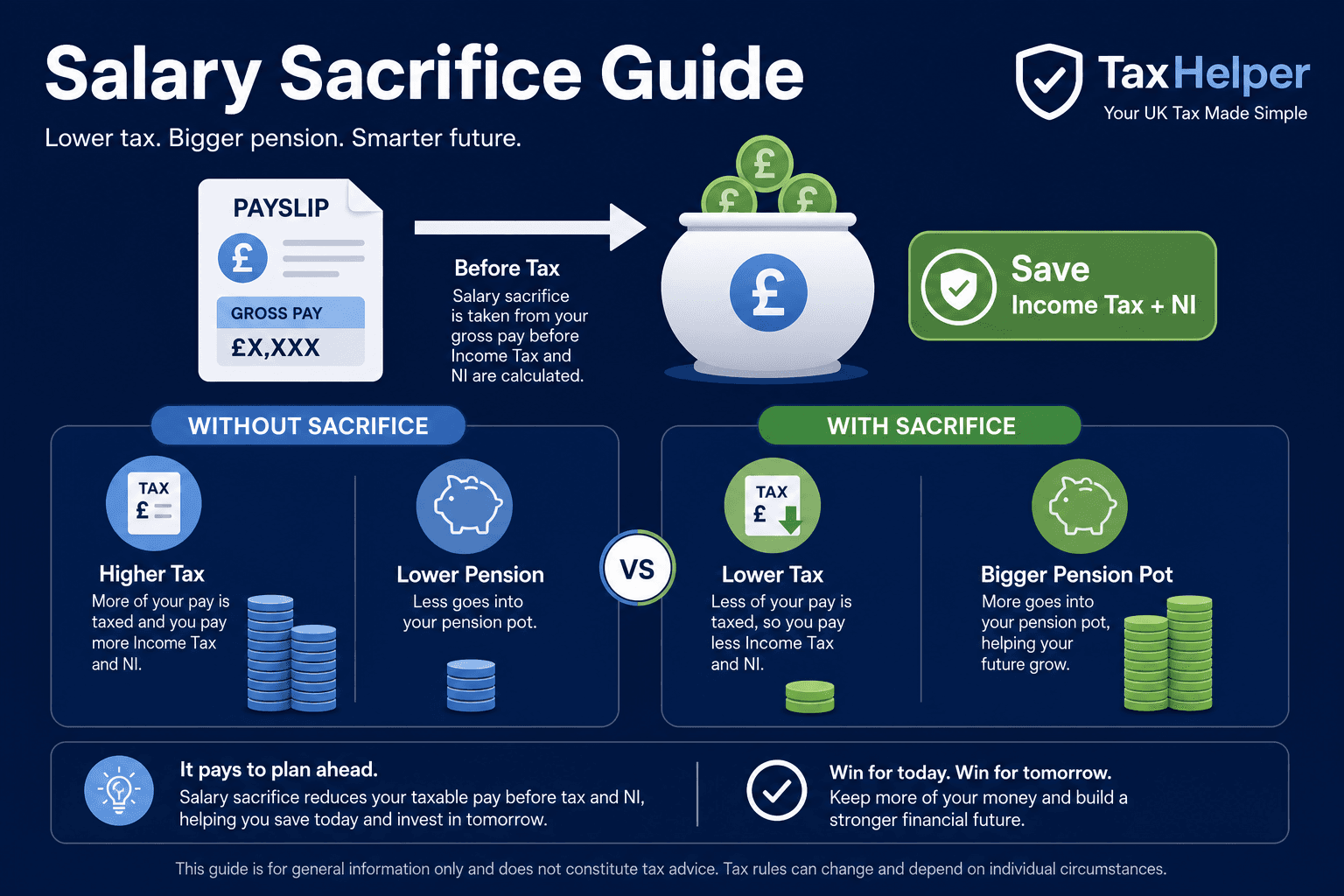

Salary sacrifice reduces your gross pay before tax is calculated, saving both Income Tax and National Insurance. It is one of the most tax-efficient ways to boost pension savings, get an EV, or access other employer benefits.

At a glance

- ✓Sacrifice is deducted before tax, saving 20–45% in income tax plus 8% employee NI

- ✓A £200/month sacrifice costs a basic-rate taxpayer only £144 in net pay

- ✓Employers also save 15% NI — many pass this saving into your pension

- ✓Check impact on mortgage applications, statutory pay, and life assurance before signing

How salary sacrifice works

You agree with your employer to reduce your contractual salary in exchange for a non-cash benefit of equal value. Because the benefit comes from pre-tax salary, you save Income Tax at your marginal rate plus 8% employee NI (for earnings below £50,270).

Employers save 15% employer NI on the sacrificed amount. This means salary sacrifice arrangements often cost employers nothing — and can actually save them money while improving your benefits package.

Worked example

Scenario: Salary £40,000, sacrifice £3,000/year into pension (basic-rate taxpayer).

| Item | Without sacrifice | With sacrifice | Saving |

|---|---|---|---|

| Gross salary | £40,000 | £37,000 | — |

| Income Tax | £5,486 | £4,886 | £600 |

| Employee NI | £2,234 | £1,994 | £240 |

| Net take-home reduction | — | — | £840 |

| Pension contribution | £0 | £3,000 | — |

| Employer NI saved | — | — | £450 |

Net cost: £3,000 sacrifice reduces take-home by only £2,160 (£3,000 − £840 in tax/NI savings). Effective cost: 72p per £1 in pension.

What can be sacrificed?

Pension contributions

Most common use. Applies to workplace defined contribution pensions. Annual allowance limits still apply (£60,000 gross in 2026/27).

Cycle to Work

Up to £1,000 (or £1,500 for e-bikes) in vouchers for a bicycle and safety equipment, spread over 12 months.

Electric vehicles (EV)

EV salary sacrifice for a company car. BiK tax rate for pure EVs is just 3% in 2026/27, making this very tax-efficient.

Childcare vouchers

Legacy scheme closed to new entrants since October 2018. If already enrolled, existing members can continue.

Salary sacrifice vs personal SIPP

| Factor | Salary sacrifice | SIPP (relief at source) |

|---|---|---|

| NI saving (employee) | Yes — 8% | No |

| NI saving (employer) | Yes — 15% | No |

| Higher-rate relief | Automatic via lower gross | Claim via Self Assessment |

| Flexibility | Limited by employer scheme | Full flexibility |

| Mortgage impact | May reduce qualifying pay | No impact |

Statutory pay: Salary sacrifice reduces the "contractual pay" figure used to calculate Statutory Maternity Pay, Sick Pay, and redundancy — particularly important if you plan to start a family or change roles soon.

Common questions

Does salary sacrifice reduce my take-home pay?

Yes, but less than you might expect. For a basic-rate taxpayer, sacrificing £200/month saves £56 in tax and NI. So net take-home reduces by £144, while your pension (or other benefit) receives £200.

Can salary sacrifice affect my mortgage application?

Potentially. Lenders typically look at your contractual (post-sacrifice) salary for affordability calculations. Your P60 will show the lower figure. Discuss with your mortgage broker before arranging large sacrifice amounts.

Is salary sacrifice available at all employers?

No. Salary sacrifice is a voluntary arrangement between you and your employer. Your employer must agree to offer it and update your contract. Many large employers offer it for pensions; not all offer it for other benefits.

Does employer NI saving always benefit me?

Not automatically. Some employers pass all or part of their NI saving into your pension or benefit. Others keep it. Ask your HR or payroll team whether the employer NI saving is shared.

Sources

See your salary after sacrifice

Model the exact effect of salary sacrifice on your take-home pay, tax code, and pension contributions.

Salary calculator