IR35 Explained

Last reviewed: April 2026

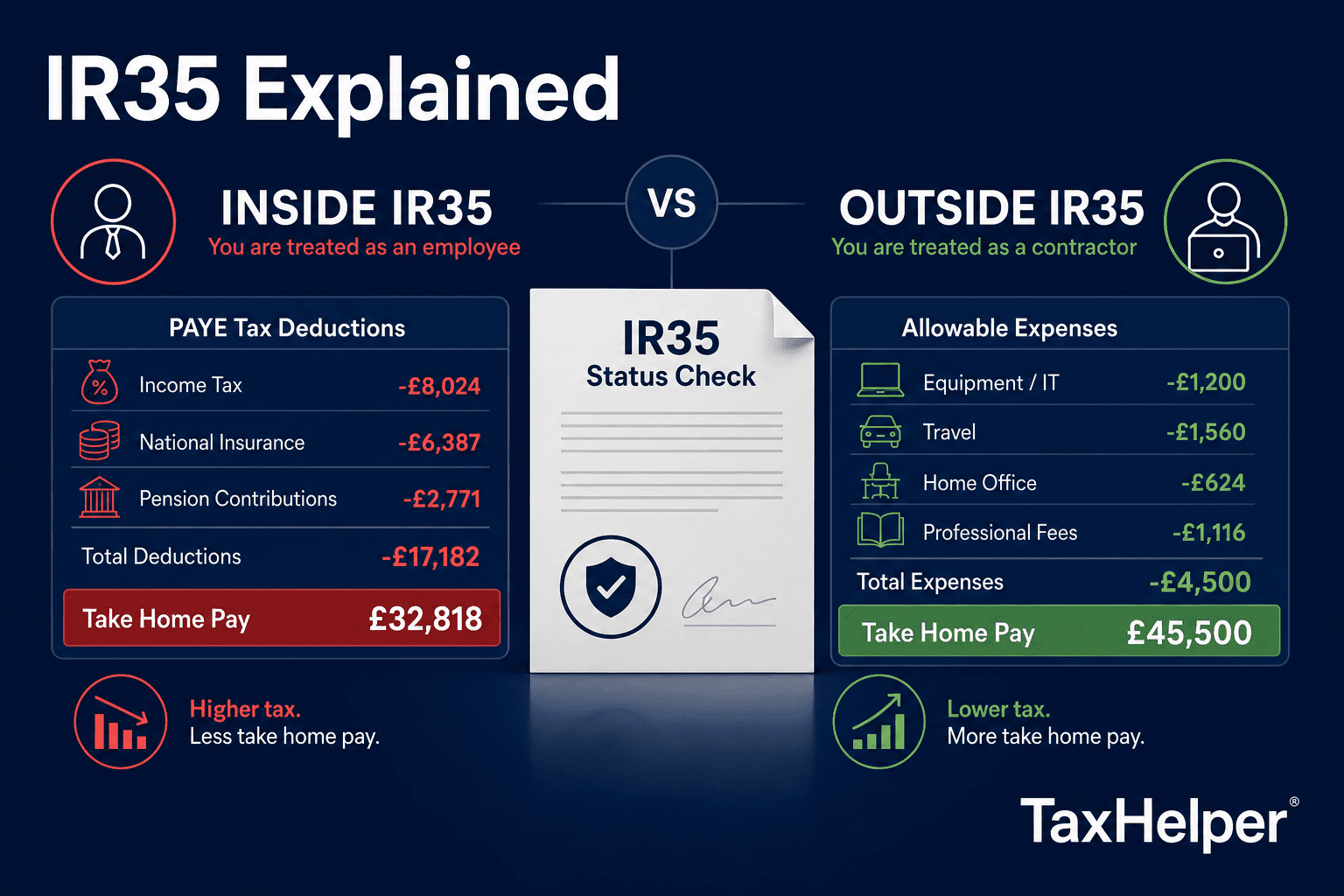

IR35 — officially the "off-payroll working rules" — determines whether contractors working through a limited company should be taxed as employees. Getting it wrong carries substantial penalties.

At a glance

- ✓Inside IR35 means your fee income is taxed like a salary (PAYE + NI on the whole amount)

- ✓Since April 2021, medium and large companies decide IR35 status — not the contractor

- ✓Outside IR35: you take a small salary + dividends, paying less overall tax

- ✓HMRC's CEST tool helps assess status — HMRC will stand by correct CEST results

Inside vs outside IR35

| Factor | Inside IR35 | Outside IR35 |

|---|---|---|

| Tax treatment | Salary-equivalent via PAYE | Salary + dividends |

| NI on contract income | Employee + employer NI on all | NI on salary portion only |

| Expenses deduction | Very limited | Normal business expenses |

| IR rate for equivalent £60k | ~£37,000 net | ~£44,000 net |

| Who determines status | End client (medium/large co) | End client or contractor (small co) |

Worked example — £60,000 contract

A contractor bills £60,000 through a limited company. Corporation tax (25%) applies to profit either way, but:

Inside IR35

- Deemed salary: ~£48,000 (after employer NI)

- Income Tax: ~£8,946

- Employee NI: ~£2,834

- Employer NI: ~£6,450

- Net take-home: ~£37,800

Outside IR35

- Salary: £12,570, dividends: £40,000+

- Income Tax: ~£4,000

- Dividend tax: ~£2,625 (8.75%)

- NI: ~£0 (below PT after salary)

- Net take-home: ~£44,000+

Approximate figures; exact amounts depend on expenses, pension contributions, and other income.

How HMRC decides — the three key tests

Substitution

Can you send a substitute to do the work instead of you? A genuine right of substitution is strong evidence of outside IR35.

Control

Does the client control how, when, and where you work? Employee-like control points toward inside IR35.

Mutuality of obligation

Is the client obliged to offer work and are you obliged to accept it? This mutual obligation is a key employment indicator.

CEST limitations: HMRC's CEST tool does not currently assess mutuality of obligation — a significant limitation recognised by tax tribunals. Always take professional advice for complex or high-value contracts.

Common questions

What does 'inside IR35' mean?

Inside IR35 means HMRC considers your engagement similar to employment. Your income from that contract is treated like a salary — subject to PAYE Income Tax and National Insurance on the full fee, with no ability to take dividends tax-efficiently.

Who decides if a contract is inside or outside IR35?

For public sector and medium/large private sector clients (since April 2021), the end client decides. For small private sector clients, the contractor's personal service company (PSC) decides. HMRC's CEST tool can assist but is not legally binding.

Can I appeal an inside IR35 determination?

Yes. Clients must issue a Status Determination Statement (SDS) explaining their decision. Contractors can trigger a formal disagreement process. If unresolved, the matter may go to tribunal.

What is the CEST tool?

Check Employment Status for Tax (CEST) is HMRC's free online tool to help assess whether a contract falls inside or outside IR35. HMRC agrees to stand by CEST results if you answer honestly and the contract matches your working arrangements.

Sources

Model your contractor tax position

Use our self-employed calculator to estimate Income Tax, NI, and take-home for different salary and dividend combinations.

Self-employed calculator