Dividends vs Salary

Last reviewed: April 2026

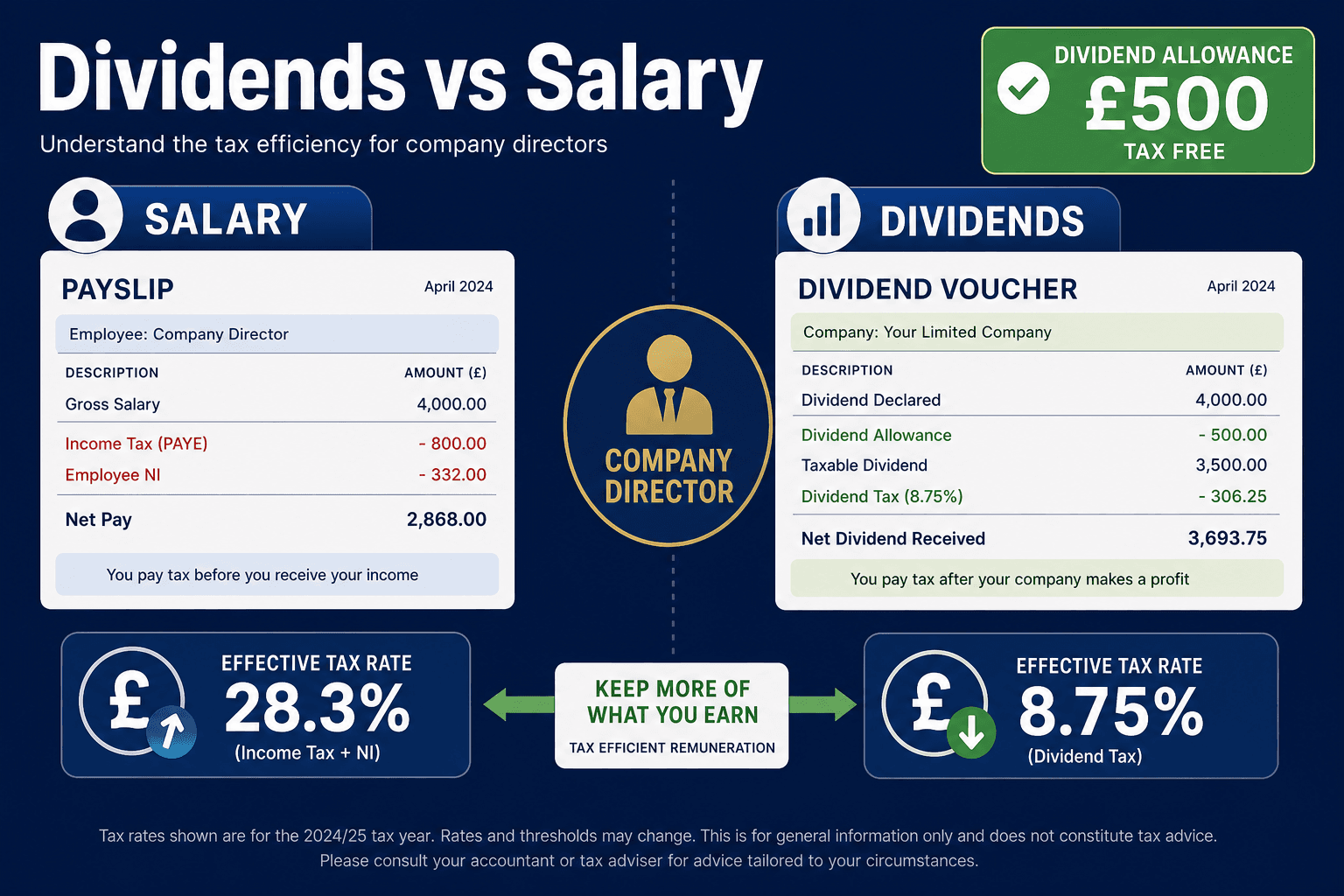

Most limited company directors take a low salary topped up with dividends to minimise their total tax and NI bill. Here is how the maths works in 2026/27 — and when a higher salary might actually be better.

At a glance

- ✓Dividends are not subject to NI — saving up to 23% vs salary (20% tax + 8% NI − employer NI)

- ✓The dividend allowance is £500 in 2026/27 — above that, rates are 8.75% / 33.75% / 39.35%

- ✓Optimal director salary is typically £12,570 (with Employment Allowance) or £5,000 (without)

- ✓Corporation Tax (25%) is paid before dividends — factor this into your total tax calculation

Dividend tax rates 2026/27

| Band | Total income | Dividend tax rate |

|---|---|---|

| Allowance | First £500 of dividends | 0% |

| Basic rate | Up to £50,270 total income | 8.75% |

| Higher rate | £50,271–£125,140 | 33.75% |

| Additional rate | Over £125,140 | 39.35% |

Worked example — director taking £60,000

Company profit before director pay: £75,000. Director wants to extract £60,000. Optimal structure:

Excludes Corporation Tax (25%) on company profit. Assumes Employment Allowance is available.

When a higher salary beats dividends

Pension contributions

Employer pension contributions are a business expense, reducing Corporation Tax. Salary-linked contributions can significantly boost pension savings.

Mortgage applications

Many lenders require 2–3 years of self-employed accounts showing salary. A higher salary makes affordability easier to evidence.

Maternity/paternity pay

Statutory pay is calculated from salary, not dividends. A very low salary means minimal statutory pay entitlement.

State Pension record

Salary above the Lower Earnings Limit (£6,396) counts toward NI years. Very low salary risks gaps in your State Pension record.

Common questions

Why do directors take dividends instead of a full salary?

Dividends are not subject to National Insurance (employer or employee). At the basic-rate, dividend tax is 8.75% versus 20% income tax + 8% employee NI on salary, making dividends significantly more tax-efficient once profits are in the company.

What is the 2026/27 dividend allowance?

The tax-free dividend allowance is £500 for 2026/27 (reduced from £1,000 in 2023/24 and £2,000 previously). Above the allowance, dividends are taxed at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate).

What is the optimal director salary for 2026/27?

Most accountants recommend a salary at the Secondary Threshold (£5,000/year in 2026/27) if the company has no Employment Allowance, or at the Primary Threshold (£12,570/year) if it does. This minimises NI while counting toward qualifying NI years for State Pension.

Are there any downsides to taking dividends?

Yes. Dividends do not count as earnings for pension contribution purposes. Mortgage applications use salary (not dividends) for affordability in some cases. And dividends require the company to have distributable profits after Corporation Tax.

Sources

Estimate your self-employed tax

Model your salary and dividend mix to see the optimal take-home for your situation.

Self-employed calculator