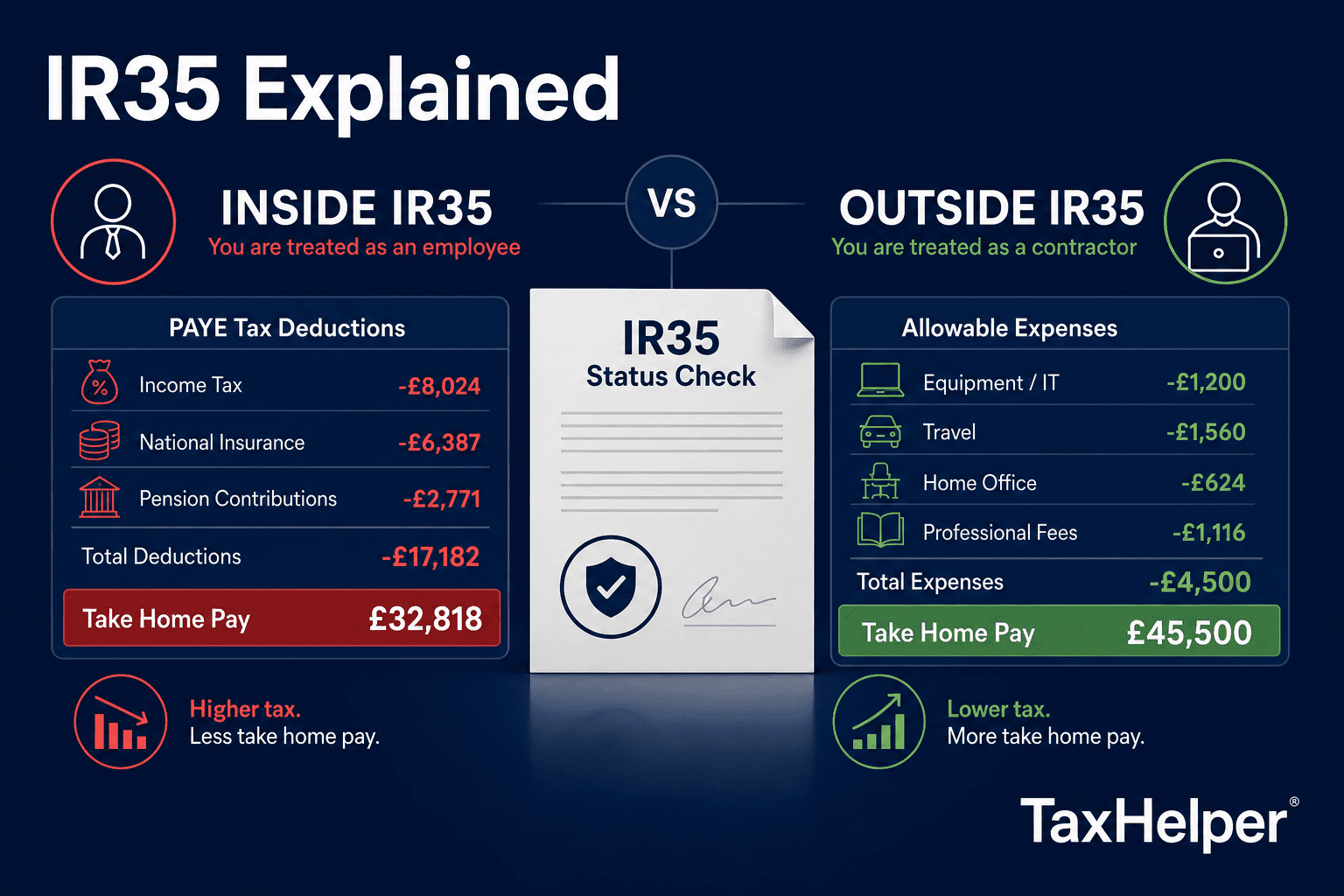

Employed vs Self-Employed:

Tax Comparison 2026/27

Last reviewed: April 2026

Employment and self-employment are taxed differently. Here is a side-by-side breakdown of income tax, National Insurance, expenses and take-home pay.

At a glance

- ✓Both employed and self-employed pay income tax at the same rates (20%/40%/45%)

- ✓Self-employed Class 4 NI (9%) is slightly higher than employee NI (8%), but you pay no employer NI (15%)

- ✓Self-employed people can deduct a much wider range of business expenses

- ✓Employment offers statutory sick pay, holiday pay and often employer pension contributions — self-employment does not

Take-home pay: employed vs self-employed

At the same gross income level, employed and self-employed take-home pay is surprisingly close. The self-employed generally pay slightly more NI in aggregate — but can often reduce their taxable profits with legitimate expenses.

| Gross income | Employed take-home | SE take-home | Difference |

|---|---|---|---|

| £25,000 | £20,232 | £19,857 | -£375 |

| £35,000 | £27,232 | £26,332 | -£900 |

| £50,000 | £37,832 | £36,482 | -£1,350 |

| £70,000 | £48,232 | £47,932 | -£300 |

Approximate figures assuming no employer pension contributions and no business expense deductions. Use the calculators for a precise comparison.

Side-by-side: key differences

| Topic | Employed | Self-employed |

|---|---|---|

| Income tax | PAYE — deducted automatically | Self Assessment — pay by 31 Jan/31 Jul |

| National Insurance | 8% employee NI (£12,570–£50,270) | 9% Class 4 NI on profits (£12,570–£50,270) |

| Employer NI | Paid by employer (15%) | None — you pay both sides effectively |

| Business expenses | Very limited (HMRC strict) | Full deduction if wholly & exclusively for business |

| Pension relief | Employer contributions common | Personal/SIPP contributions; no employer match |

| Holiday/sick pay | Statutory minimums guaranteed | None — self-insure |

| Filing requirement | Usually none | Annual Self Assessment required |

Pros and cons for tax purposes

Employment advantages

- Employer pays NI — saves you 15% on your gross

- Employer pension contributions (free money)

- Statutory sick pay and holiday pay

- No self-filing requirement (usually)

- Very limited expense deductions

Self-employment advantages

- Deduct real business costs before calculating tax

- More control over timing of income (smoothing)

- Can choose pension structure (SIPP/SSAS)

- No statutory sick or holiday pay

- Must file Self Assessment annually

Frequently asked questions

Frequently asked questions

Is it cheaper to be self-employed than employed at the same income?

It depends on income level and allowable expenses. At equivalent gross income, a sole trader typically pays slightly less NI than an employee (9% vs 8% employee + 15% employer, though employer NI does not come from your gross pay). However, self-employed people miss out on employer pension contributions and statutory pay.

Can I be employed and self-employed simultaneously?

Yes — this is very common. You pay employee NI through PAYE on your employment income and Class 4 NI on self-employment profits. There are annual limits on total NI to prevent paying on the same earnings twice, which Self Assessment reconciles.

What expenses can self-employed people claim that employees cannot?

Self-employed people can deduct costs that are wholly and exclusively for their business: equipment, software, professional subscriptions, business travel, marketing, accountancy fees and a proportion of home costs (if working from home regularly). Employees can only claim for expenses their employer has not reimbursed and HMRC must agree are necessary.

Do self-employed people get a Personal Allowance?

Yes — everyone gets the same £12,570 Personal Allowance regardless of employment status. Self-employed profits below £12,570 are not taxed. Above that, income tax applies at the same rates as for employees.