Becoming Self-Employed:

Tax Survival Guide

Last reviewed: April 2026

Going self-employed puts you in charge of your own tax. Here is how to register, what to set aside, and how to navigate your first Self Assessment.

At a glance

- ✓Register with HMRC using a CWF1 form — by 5 October after your first trading year

- ✓Self-employed people pay income tax + Class 4 NI (9%) on profits between £12,570 and £50,270

- ✓Set aside 20–30% of gross income immediately — HMRC will want it in January

- ✓You can earn up to £1,000 tax-free via the Trading Allowance

Five steps to get your tax right from the start

- 1

Register as self-employed with HMRC

Use the online CWF1 form at gov.uk. You must register by 5 October after the tax year you started trading. Late registration can result in a penalty.

- 2

Get a UTR number

HMRC issues your Unique Taxpayer Reference (UTR) — a 10-digit number used for all Self Assessment correspondence. It arrives by post within 10 working days of registering.

- 3

Set aside 20–30% of profits for tax and NI

There is no employer deducting tax on your behalf. A good rule of thumb: set aside 20% of profits for income tax (if a basic-rate taxpayer) plus 9% for Class 4 NI. More if you earn over £50,270.

- 4

Keep records of all income and expenses

HMRC requires you to keep records for at least 5 years after the 31 January deadline of the relevant tax year. Digital records make this easier — many use free/paid accounting software.

- 5

File your first Self Assessment by 31 January

For the tax year ending 5 April 2026, the filing deadline is 31 January 2027 for online returns. Paper returns must be submitted by 31 October 2026.

Self-employment tax rates 2026/27

As a sole trader, you pay income tax and Class 4 National Insurance on your net profits (after allowable expenses). Class 2 NI was abolished in April 2024.

| Profit band | Income tax | Class 4 NI | Total |

|---|---|---|---|

| Up to £12,570 | 0% | 0% | 0% |

| £12,571–£50,270 | 20% | 9% | 29% |

| £50,271–£125,140 | 40% | 2% | 42% |

| Over £125,140 | 45% | 2% | 47% |

Class 4 NI lower profits limit is £12,570. Upper profits limit is £50,270. Above £50,270, Class 4 NI rate drops to 2%.

Payments on Account: the first-year cash flow shock

In your first year of filing Self Assessment, HMRC asks you to pay your tax bill plus 50% upfront towards next year all on 31 January. This 'Payments on Account' system means your first Self Assessment bill is typically 150% of what you actually owe.

Example: First-year tax bill of £4,000. On 31 January you pay £4,000 (actual) + £2,000 (first payment on account) = £6,000. Then a second £2,000 on 31 July.

Full Payments on Account guideFrequently asked questions

Frequently asked questions

When do I need to register as self-employed?

You must register by 5 October after the end of the tax year in which you started trading. So if you started trading in August 2025 (tax year 2025/26), the deadline is 5 October 2026. Registering early is better — you will get your UTR sooner and have more time to prepare.

What if I am employed and self-employed at the same time?

Very common. You pay PAYE tax and NI on your employment as normal, and additionally file a Self Assessment return for your self-employment income. Your Class 4 NI threshold is shared across both — you do not pay Class 1 and Class 4 NI on the same earnings twice.

What is the Trading Allowance?

You can earn up to £1,000 from self-employment completely tax-free under the Trading Allowance. If your gross trading income is below £1,000, you do not need to file a Self Assessment return for that income. Above £1,000, you can either claim the £1,000 allowance or deduct actual expenses — whichever is better.

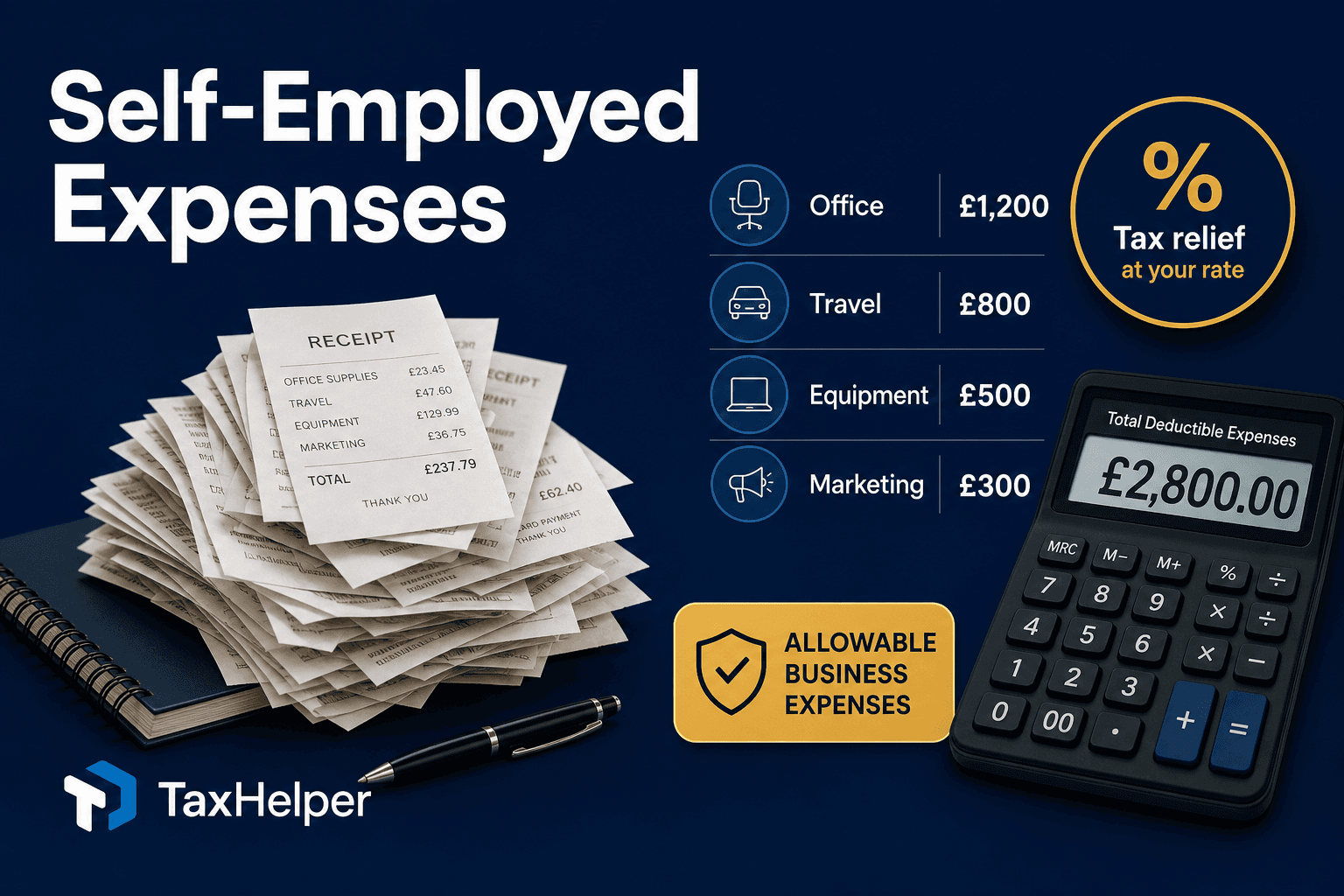

What counts as an allowable business expense?

Costs that are wholly and exclusively for your business: equipment, software, professional subscriptions, business travel, home office costs (using the simplified flat rate or actual method), advertising and marketing, accountancy fees. Personal costs are not allowable even if you use them partly for work — unless you can clearly apportion them.