Redundancy Pay

and Tax in the UK

Last reviewed: April 2026

The first £30,000 of a genuine redundancy payment is completely tax-free. But not everything in a redundancy package qualifies. Here is what is taxable, what is not, and how to calculate your net payment.

At a glance

- ✓Statutory redundancy pay and ex-gratia payments up to £30,000 are tax-free

- ✓Payment in lieu of notice (PILON) is fully taxable as earnings

- ✓Holiday pay accrued but untaken is also taxable

- ✓Amounts above £30,000 are taxed at your marginal rate and attract NI

What is taxable and what is not in a redundancy package

Statutory Redundancy Pay (up to £30,000 combined)

Always tax-free. Calculated using a government formula based on age, service and capped weekly pay (£643/week in 2026/27).

Tax-freeEnhanced redundancy pay (up to £30,000 combined)

If your employer pays more than the statutory minimum, the enhancement is also tax-free — as long as the total genuine redundancy payment does not exceed £30,000.

Tax-freePay in lieu of notice (PILON)

Fully taxable as employment income. Subject to income tax and National Insurance regardless of whether your contract includes a PILON clause.

TaxableHoliday pay

Payment for accrued but untaken holiday is always taxable — it is straightforward employment income.

TaxablePayments for work done

Final month's salary, overtime, commission or bonuses for work already performed are fully taxable.

TaxableRedundancy pay above £30,000

Any genuine redundancy payment above £30,000 is subject to income tax (but not NI) on the excess.

TaxableNon-cash benefits on termination

Some employer-provided benefits given on leaving — such as outplacement counselling — are exempt from tax up to certain limits.

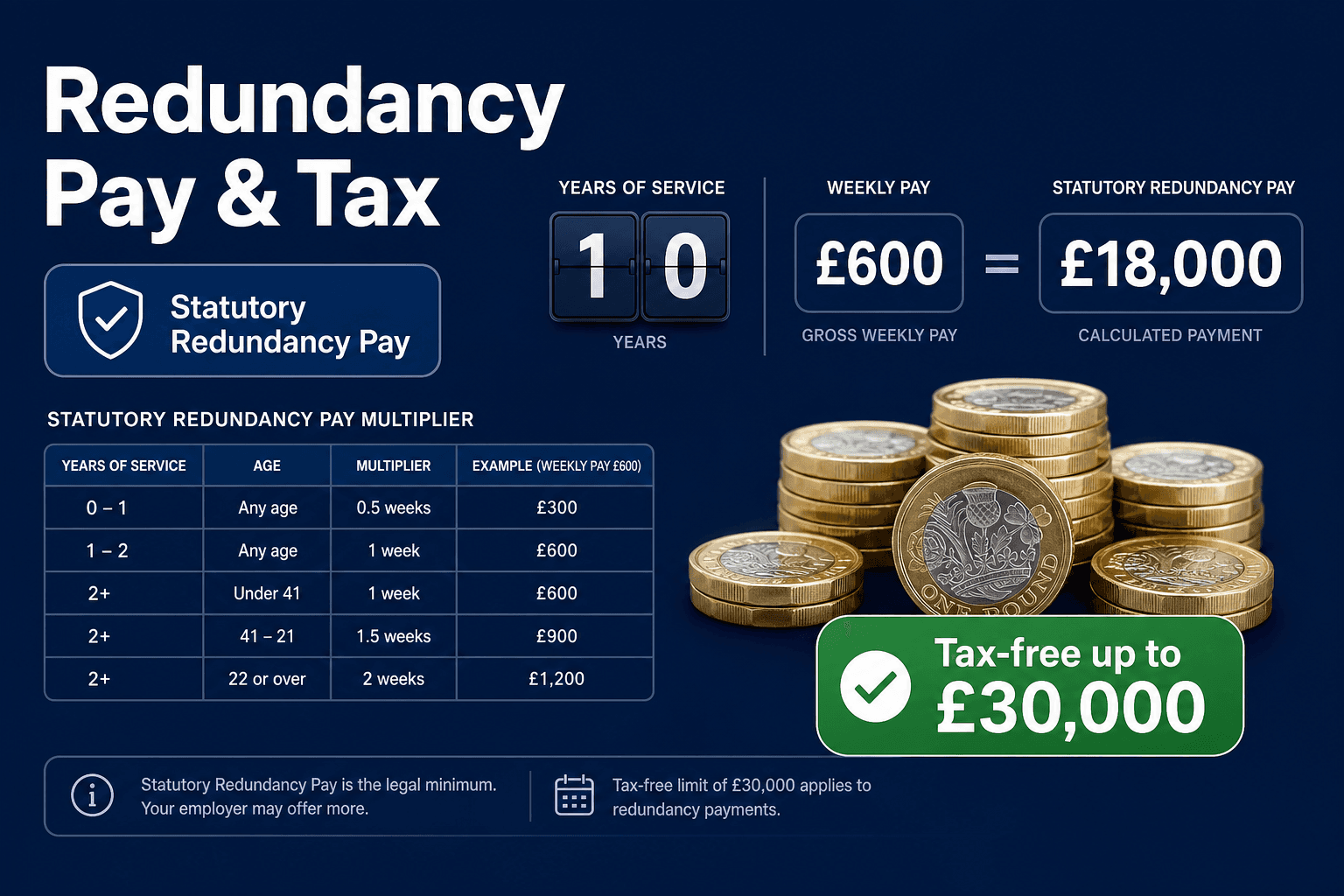

Tax-freeHow statutory redundancy pay is calculated

Statutory Redundancy Pay is based on your age, years of service (up to 20 years) and a weekly pay capped at £643 in 2026/27. The calculation is:

| Age during service | Weeks' pay per year of service |

|---|---|

| Under 22 | 0.5 weeks |

| 22 to 40 | 1 week |

| 41 and over | 1.5 weeks |

Example: 10 years service, age 38, earning £800/week

What if my redundancy payment exceeds £30,000?

The excess is subject to income tax but NOT National Insurance. This makes large redundancy payments more efficient than salary — you save 8% NI on the amount above £30,000 compared to ordinary earnings.

The taxable portion (above £30,000) is added to your other income for the year when calculating which rate band applies. If you receive a large redundancy payment late in the tax year, you may have already used up part of your basic rate band with your salary, meaning some of the excess is taxed at 40%.

One strategy: if your redundancy payment takes you over £100,000 in total income for the year, consider making a personal pension contribution to reduce your adjusted net income — this can restore your personal allowance and save significant tax at the marginal 60% rate.

Frequently asked questions

Is redundancy pay taxable in the UK?

Genuine redundancy payments up to £30,000 are free of income tax and National Insurance. Anything above £30,000 is taxed as income at your marginal rate. Note that regular pay, holiday pay and pay in lieu of notice (PILON) are always fully taxable, regardless of the £30,000 exemption.

What is the statutory redundancy pay limit?

Statutory Redundancy Pay is calculated using a formula based on your age, length of service and weekly pay. The weekly pay is capped at £643 per week (2026/27 rate). Maximum total statutory redundancy pay is 30 weeks at the capped rate, so up to £19,290 — well under the £30,000 tax-free threshold.

Does redundancy pay affect my benefits or tax credits?

A lump sum redundancy payment is generally treated as capital rather than income for means-tested benefit purposes. However, if the payment is large, it could affect certain benefits. The ongoing lack of income after redundancy is what primarily affects Universal Credit and other means-tested benefits.

What is pay in lieu of notice (PILON) and is it taxed?

Pay in lieu of notice (PILON) is payment your employer gives you instead of you working your notice period. Since April 2018, all PILON payments are fully subject to income tax and Class 1 National Insurance, whether or not your contract includes a PILON clause. PILON does not count toward the £30,000 tax-free exemption.

Sources

Understand your tax position after redundancy

Our salary calculator can model your income and tax for the year, including any redundancy payment, to help you plan effectively.